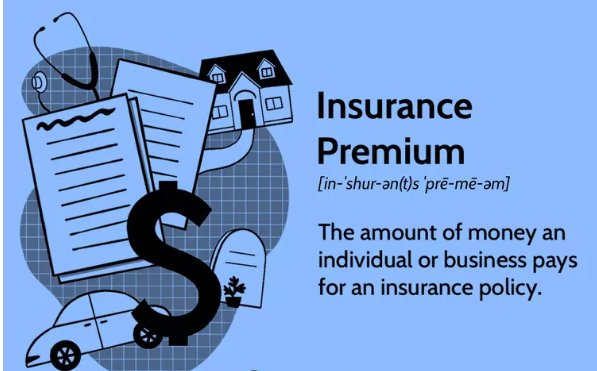

What Determines Your Home Insurance Premium?

When shopping for home insurance, you may wonder why your premium differs from others or what factors influence the cost. Home insurance providers use several key variables to assess risk and determine your rate. Understanding these factors can help you make informed decisions and even find ways to lower your premium.

1. Location of Your Home

Your home’s location is one of the biggest factors influencing your insurance premium. Insurers evaluate risks such as crime rates, weather patterns, and proximity to fire stations. You’ll likely pay a higher premium if you live in an area prone to hurricanes, wildfires, or floods. Similarly, urban areas with higher crime rates may result in increased costs.

2. Home Characteristics and Age

Your home’s age, size, and structure significantly impact your premium. Older homes may have outdated electrical or plumbing systems, increasing the risk of damage and higher claim costs. Newer homes with modern safety features, such as updated wiring, impact-resistant roofing, and smart security systems, can lower your insurance premium.

3. Coverage and Deductibles

The level of coverage you choose directly affects your premium. Higher coverage limits and additional protections (such as earthquake or flood insurance) increase costs. Conversely, opting for a higher deductible—meaning you’ll pay more out-of-pocket before insurance kicks in—can lower your premium.

4. Claims History

A history of previous claims can raise your home insurance premium. Insurers view frequent claims as a higher risk. If you’ve filed multiple claims in the past, you may face increased rates. Maintaining a claims-free record can help reduce your costs.

5. Credit Score and Financial History

In many states, insurers use credit scores to determine premiums. A higher credit score typically translates to lower rates, as it suggests financial responsibility. Conversely, lower credit scores may lead to higher premiums due to perceived higher risk.

6. Home Safety Features

Homes equipped with security systems, smoke detectors, deadbolts, and sprinkler systems may qualify for discounts. Insurers reward homeowners who invest in risk-reducing features that minimize potential claims.

7. Local Building Costs

The cost of materials and labor in your area can influence your insurance rate. If rebuilding costs are high due to inflation or supply chain issues, insurers may increase premiums to reflect potential payout amounts.

8. Bundling and Discounts

Many insurance companies offer discounts when you bundle home and auto policies or install protective measures. Shopping around and asking about available discounts can help you save on your premium.

Final Thoughts

Understanding what determines your home insurance premium can help you make smart decisions to manage costs. While some factors—like location—are beyond your control, improving home safety, maintaining a good credit score, and choosing the right coverage can lead to savings. Regularly reviewing your policy ensures you have the best coverage at the most competitive rate.