Mistakes to Avoid When Applying for a Home Loan

Buying a home is one of the most significant financial decisions you’ll make, and securing a home loan is a crucial step in that process. However, many homebuyers make mistakes that can lead to delays, higher costs, or even loan rejection. To help you navigate this journey smoothly, here are some key mistakes to avoid when applying for a home loan.

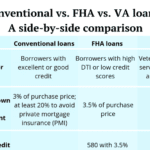

1. Not Checking Your Credit Score

Your credit score plays a major role in determining your loan eligibility and interest rate. A lower score can lead to higher interest rates or even denial of your application. Before applying, check your credit report for errors, pay down debts, and work on improving your score if needed.

2. Failing to Get Pre-Approved

Many buyers skip the pre-approval process, assuming they will qualify for a loan. However, pre-approval not only gives you a clear idea of your budget but also makes you a more attractive buyer in competitive markets. It also helps you identify any potential issues before making an offer on a home.

3. Taking on New Debt Before Closing

Lenders evaluate your debt-to-income ratio before approving your home loan. Taking on new debt, such as financing a car or opening a new credit card, can alter your financial profile and may result in loan denial at the last minute. Avoid making large purchases or opening new credit accounts until your loan has been finalized.

4. Not Comparing Lenders

Many borrowers accept the first loan offer they receive without shopping around for better rates and terms. Different lenders offer varying interest rates and loan conditions. Getting quotes from multiple lenders can help you secure the best deal, potentially saving you thousands over the life of the loan.

5. Ignoring Loan Fees and Closing Costs

The interest rate isn’t the only factor to consider. Many homebuyers overlook additional costs such as origination fees, appraisal fees, and closing costs. Request a loan estimate from your lender to understand the full cost of borrowing and avoid unexpected expenses.

6. Making Large Deposits Without Documentation

Lenders scrutinize your bank statements to ensure financial stability. Large, unexplained deposits can raise red flags and slow down the approval process. If you receive a significant deposit, be prepared to provide documentation explaining its source.

7. Underestimating Future Expenses

Many buyers focus solely on their mortgage payment without considering other homeownership costs like property taxes, homeowners insurance, maintenance, and utilities. Ensure you budget for these additional expenses to avoid financial strain.

8. Providing Inaccurate Information

Honesty is crucial when applying for a home loan. Providing false or incomplete information on your application can result in delays, higher scrutiny, or outright rejection. Ensure all details, including your income, employment history, and debts, are accurate and up to date.

9. Changing Jobs Before Closing

Lenders prefer a stable employment history, as sudden job changes can raise concerns about your ability to repay the loan. If possible, avoid changing jobs until after your loan has closed. If a job change is unavoidable, inform your lender immediately and provide any necessary documentation.

10. Not Reading the Fine Print

A home loan is a long-term commitment, and failing to understand the terms can lead to costly mistakes. Review all loan documents carefully, including interest rates, repayment terms, and penalties. If anything is unclear, ask your lender or a financial advisor for clarification before signing.

Conclusion

Applying for a home loan requires careful planning and attention to detail. By avoiding these common mistakes, you can improve your chances of securing a loan with favorable terms and move confidently toward homeownership. Take the time to educate yourself, seek professional guidance if needed, and make informed financial decisions for a successful home-buying experience.