How to Get the Best Mortgage Rate for Your Home Loan

Buying a home is one of the biggest financial decisions you’ll ever make, and securing the best mortgage rate can save you thousands of dollars over the life of your loan. Lenders determine your mortgage rate based on several factors, including your credit score, down payment, and market conditions. Here’s a step-by-step guide to help you secure the lowest possible mortgage rate.

1. Improve Your Credit Score

Your credit score is one of the most significant factors that lenders consider when determining your mortgage rate. Higher scores often lead to lower interest rates. Here’s how to boost your credit score:

- Pay Bills on Time: Late payments can negatively impact your score.

- Reduce Debt: Lower your credit utilization ratio by paying down existing debt.

- Check Your Credit Report: Review your credit report for errors and dispute any inaccuracies.

- Avoid New Credit Accounts: Opening new credit lines before applying for a mortgage can temporarily lower your score.

2. Save for a Larger Down Payment

A larger down payment reduces the lender’s risk and can result in a lower mortgage rate. Most lenders require a minimum of 3-5% down, but putting down 20% or more can help you avoid private mortgage insurance (PMI) and qualify for better rates.

3. Shop Around and Compare Lenders

Mortgage rates vary between lenders, so it’s crucial to compare multiple offers. Consider checking rates from:

- Traditional banks

- Credit unions

- Mortgage brokers

- Online lenders

Using a mortgage comparison tool or working with a broker can help you find the best deal.

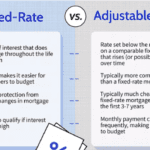

4. Consider Different Loan Types and Terms

Different types of loans come with varying interest rates. For example:

- Fixed-Rate Mortgages: Offer consistent payments over the loan term and are ideal for long-term stability.

- Adjustable-Rate Mortgages (ARMs): Start with lower rates but can increase over time.

- Government-Backed Loans: FHA, VA, and USDA loans often have competitive rates for qualified borrowers.

Additionally, shorter loan terms (e.g., 15-year vs. 30-year) usually have lower interest rates but higher monthly payments.

5. Lock in Your Rate at the Right Time

Mortgage rates fluctuate based on economic conditions. If rates are trending upwards, consider locking in a rate to secure the best deal. Many lenders offer rate locks for 30-60 days.

6. Lower Your Debt-to-Income Ratio (DTI)

Lenders assess your ability to repay the loan based on your debt-to-income ratio. To improve your DTI:

- Pay off existing debts.

- Avoid taking on new loans or credit card debt before applying.

- Increase your income if possible.

7. Negotiate Closing Costs

Some lenders offer discount points, which allow you to pay upfront fees in exchange for a lower interest rate. Be sure to negotiate closing costs and ask about lender credits to reduce your expenses.

Final Thoughts

Securing the best mortgage rate requires careful planning and research. By improving your credit score, saving for a larger down payment, shopping around, and considering various loan options, you can increase your chances of getting a competitive rate. Taking these steps will help you save money and make homeownership more affordable in the long run.

Are you in the process of buying a home? Share your experience in the comments below!